|

|||||||

Analyst Conference Call Summary

biotechnology

Biogen Inc.

BIIB

conference date: February 3, 2021 @ 5:00 AM Pacific Time

for quarter ending: December 31, 2020 (fourth quarter, Q4 2020)

Overview: Sustantial y/y revenue decline. 2021 guidance assumes approval for aducanumab. Profits were impacted by high R&D spend.

Basic data (GAAP):

Revenues were $2.85 billion, down 16% sequentially from $3.38 billion and down 22% from $3.67 billion in the year-earlier quarter.

Net income $358 million, down 49% sequentially from $0.70 billion and down 75% from $1.44 billion in the year-earlier quarter.

EPS (earnings per share, diluted) were $2.32, down 48% sequentially from $4.46 and down 71% from $8.08 year-earlier.

Guidance:

Full year 2021 revenue expected between $10.45 and $10.75 billion. Non-GAAP diluted EPS between $17.00 and $18.50. Capital expenditures to be between $375 million and $425 million. "This financial guidance assumes aducanumab, an investigational treatment for Alzheimer's disease, will be approved in the U.S. by June 7, 2021, although uncertainty remains on the FDA decision." Also assumes a significant decline in Tecfidera revenue due to generic competition.

Conference Highlights:

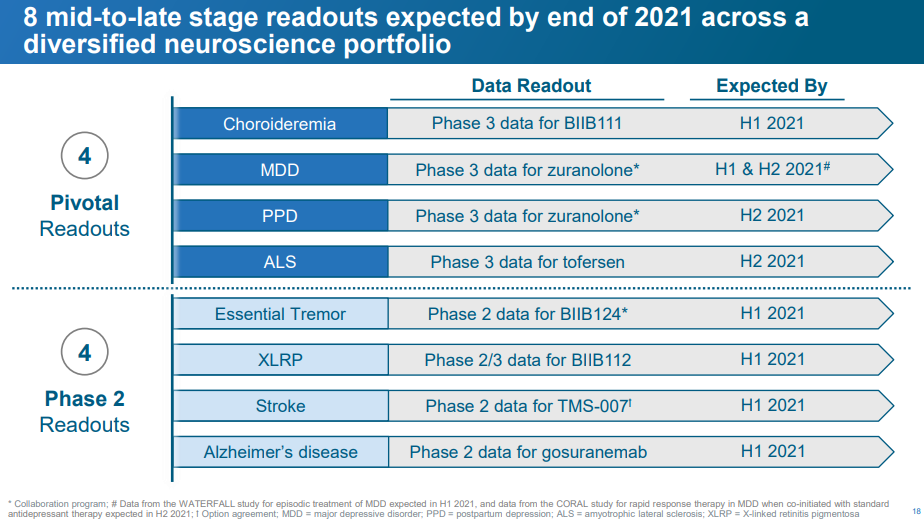

CEO Michel Vounatsos said: "Although we expect a financial reset in 2021 primarily due to the entry of Tecfidera generics, we believe that 2021 has the potential to be a transformative year for our pipeline with an anticipated regulatory decision in the U.S. on aducanumab for Alzheimer's disease in June as well as pivotal trial readouts in postpartum depression, major depressive disorder, ALS, and choroideremia. I'm proud of all that we have achieved in a challenging year, while also accelerating our actions on health and climate as well as diversity and inclusion." Believes results support aducanumab approval. Vumerity has become the leader in new oral MS prescriptions.

In Q4 2020 Biogen entered into a collaboration with Sage Therapeutics jointly develop and commercialize zuranolone (SAGE-217) for major depressive disorder, postpartum depression, and other psychiatric disorders and SAGE-324 for essential tremor and other neurological disorders. Under the agreement, Biogen made an $875 million upfront payment and an equity investment of $650 million and may pay up to $1.6 billion in potential milestone payments, profit sharing and royalties.

The FDA advisory committee recommended against approval of aducanumab. On January 29, 2021 the FDA PDUFA date of March 7, 2021 was moved to June 7, 2021 following submission of additional data and analysi. Applied in EU in October and Japan. Making preparations for expanded manufacturing. In March 2020 the first patient was dosed in the aducanumab re-dosing study, EMBARK, a global re-dosing clinical study designed to evaluate aducanumab in eligible Alzheimer's disease patients who were actively enrolled in prior aducanumab studies. Data indicates aducanumab may slow the decline of patients. Started talking to payers about pricing the drug if it is approved. Preparing to file in EU and Japan. Also expanding the Alzheimer's program with other potential therapies.

The FDA approved intramuscular injection of Plegridy for multiple sclerosis on February 1, 2021.

In Q4 2020 Biogen entered into a collaboration and licensing agreement with ViGeneron, to develop gene therapy products based on adeno-associated virus (AAV) vectors to treat inherited eye diseases. ViGeneron will be eligible to receive milestone payments as well as tiered royalties

Eight more mid to late stage data readouts are expected by the end of 2021. The Phase 3 readouts include tofersen for SOD1 ALS and BIIB111 for choroideremia.

In October 2020 Biogen entered into a collaboration with Scribe Therapeutics to develop and commercialize CRISPR-based therapies for amyotrophic lateral sclerosis (ALS). Scribe will receive a $15 million upfront payment and may be eligible to receive up to $400 million in milestones as well as tiered high single digit to sub-teen royalties,

The EMA in October 2020 accepted the MAA SB11, a proposed biosimilar referencing Lucentis (ranibizumab), an anti-VEGF (vascular endothelial growth factor), for retinal vascular disorders.

Samsung Bioepis and Biogen announced that the FDA accepted for review the BLA for SB11, a biosimilar referencing Lucentis (ranibizumab). Ranibizumab is an anti-VEGF therapy for retinal vascular disorders.

In October 2020 Biogen announced that the Phase 2 AFFINITY study of opicinumab (anti-LINGO) in MS did not meet its primary or secondary endpoints and that Biogen has discontinued development. However, will continue to research remylinization.

In Q4 2020 Biogen entered into strategic collaboration with Atalanta, for new treatment options for neurodegenerative disease, to develop RNAi therapeutics for multiple CNS targets for neurodegenerative diseases, including Parkinson's disease and Alzheimer's disease.

Non-GAAP net income was $706 million, down 49% sequentially from $1.39 billion and down 53% from $1.49 billion year-earlier. Non-GAAP EPS was $4.58, down 48% sequentially from $8.84 and down 45% from $8.34 year-earlier.

Total product revenue was $2.30 billion, down 32% sequentially from $3.38 billion and down 22% from $2.92 billion year-earlier. That excludes the Rituxan revenue, royalties and other revenue.

Therapy Revenue in Millions |

Q4 2020 |

Q3 2020 |

Q4 2019 |

y/y % |

| Tecfidera | $647 | $953 | $1,167 | -45% |

| Vumerity | 39 | 15 | 6 | 550% |

| Avonex + Plegridy | 456 | 474 | 516 | -12% |

| Tysabri | 475 | 516 | 473 | 0% |

| Fampyra | 25 | 27 | 26 | -4% |

| Spinraza | 498 | 495 | 543 | -8% |

| Benepali | 118 | 124 | 126 | -6% |

| Imraldi | 54 | 56 | 52 | 4% |

| Flixabi | 26 | 27 | 18 | 44% |

| Fumaderm | 3 | 3 | 4 | -25% |

| Rituxan*+Gazyva royalty | 217 | 288 | 396 | -45% | Ocrevus royalty | 202 | 272 | 205 | -1% |

| Other** | 132 | 126 | 146 | -10% |

* unconsolidated joint business revenue, Anti-CD20 products

** mainly contract manufacturing

Cash and equivalents (including marketable securities) balance ended at $3.38 billion, down sequentially from $4.59 billion. $7.4 billion notes payable. $1.6 billion was spent to repurchase shares, of a new $5 billion authorized. $367 million cash outflow from operations. $86 million cap ex. $453 million free cash outflow. Q4 cash flow was negatively impacted by the upfront payments to Denali and Sage and the equity premium paid to Sage.

Cost of sales was $491 million. Research and development expense was $1.73 billion. Selling, general and administrative expense $806 million. Amortization of acquired intangible assets $249 million. Collaboration profit sharing $66 million. Gain on fair value remeasurement of contingent consideration $63 million. Gain on divestiture $93 million. Total cost and expenses $3.18 billion. Leaving income from operations of negative $331 million. Other income $684 million. Income taxes $13 million. Equity in loss of investee, $18 million.

In September 2020 first patient dosed in Phase 3 AHEAD 3-45 clinical study of BAN2401, an anti-amyloid beta antibody, in individuals with preclinical Alzheimer's disease, collaborating with Eisai.

BIIB 054 Phase 2 Parkinson's study did not meet goals, so is being discontinued as of Q1 2021.

BIIB067 completed Phase 3 trial enrollment for SOD1 ALS, with initial data due by the end of 2021.

BIIB059 Phase 2 results for CLE (cutaneous lupus erythematosus) produced positive results in Q2 2020. Plans Phase 3 study to launch in H1 2020. Plans Phase 3 dapirolizumab pegol for systemic lupus erythematosus trial in Q3 2020.

BIIB122 Phase 1b met targets for Parkinson's in Q4 2020; late stage trial planned by end of 2021.

BIIB074 Phase 2 for small fiber neuropathy is enrolling. BIIB074 (vixotrigine)for trigeminal neuralgia Phase 3 initiation now planned.

TMS-007 completed Phase 2 enrollment for acute ischemic stroke in Q4 2020.

Source: Biogen Q4 2020 slides

See also the Biogen product pipeline. The entire pipeline includes 27 clinical programs. 10 mid to late stage trial readouts are expected by the end of 2020.

Full year 2020 revenue was $13.44 billion. GAAP net income was $4.00 billion. GAAP EPS was $24.80. Non-GAAP EPS $33.73

Q&A summary:

Design of Response study? Spinraza study enrolls about 60 patients who had suboptimal responses to gene therapy. Two year study, motor milestone outcomes.

Decision to include aducanumab approval in guidance? It reflects on how we see the business moving forward. We are engaging with stakeholders about price.

Aducanumab FDA data requests details? Requests are normal. The response with data and analysis led to the PDUFA delay. We do not want to provide specifics.

SG&A guidance? We budgetted for a major launch of aducanumab. We are resourcing to win. If we do not receive aducanumab approval, we would do our best to eliminate the SGA for that.

Embark complicated analysis question? We are still enrolling patients, should complete in first half.

BIIB092, anti-tau? We are looking for an effect on progression of early stage patients. Phase 1 showed decrease in tau. Hope to block spread of tau from cell to cell. Will use typical clinical outcome measures.

Growth 2022 and beyond without aducanumab? We believe we can grow the company long term. 33 programs, 8 readouts in 2021. The core business is solid and we have cash to compliment the pipeline.

Lilly results are encouraging for the amyloid hypothesis. But it was a small, 200-300 patient study.

Number of MRIs if aducanumab approved? MRI is useful for monitoring aria, and frequency will be set by regulators.

Spinraza trends, competition? We are please with 2020 revenue despite Covid, which caused the majority of impact. Some sites are closed, some patients are afraid to go for their doses. There was some switching, which peaked in September, but some are switching back for efficacy or side effects. We are still growing outside the U.S. The oral competitor is convenient, but we believe Spiraza is more effective.

The concept of down dosing after plaque removal is an interesting one. But it needs study, as we have seen patients regress after stopping aducanumab.

Advisory Committee statement about specificity of antibodies for amyloid? V. Lilly? This was a problem with earlier antibodies. You have to have anti-amyloid antibodies that will remove existing plaque, which earlier molecules did not do well. The next generation of antibodies should target the plaque better, for early stage patients.

OpenIcon

Analyst Conference Summaries Main Page

Biogen Investor Relations page

Openicon Biogen main page

More Analyst Conference Pages:

| AGEN |

| AGIO |

| ALNY |

| ALXN |

| AMAT |

| AMGN |

| APRE |

| ARWR |

| BMY |

| CLDX |

| DRNA |

| EPZM |

| GILD |

| GLYC |

| INCY |

| INO |

| IONS |

| ISRG |

| MCHP |

| MRNA |

| PLX |

| REGN |

| RNA |

| SGEN |

| SYRS |

| TTPH |

| VBLT |

| VSTM |

| XLRN |

Disclaimer: Our analyst summaries may include both our condensations of statements made by company representatives and my own analysis. They are not covered by any warranty. I cannot guarantee anything said by company representatives is true. I try not to make errors, but it is possible. These are my personal notes, which I am sharing with the investment community, not financial advice.

Copyright 2021 William P. Meyers